Contents

Audio Podcast on Investment Time Horizon: A Simple Guide

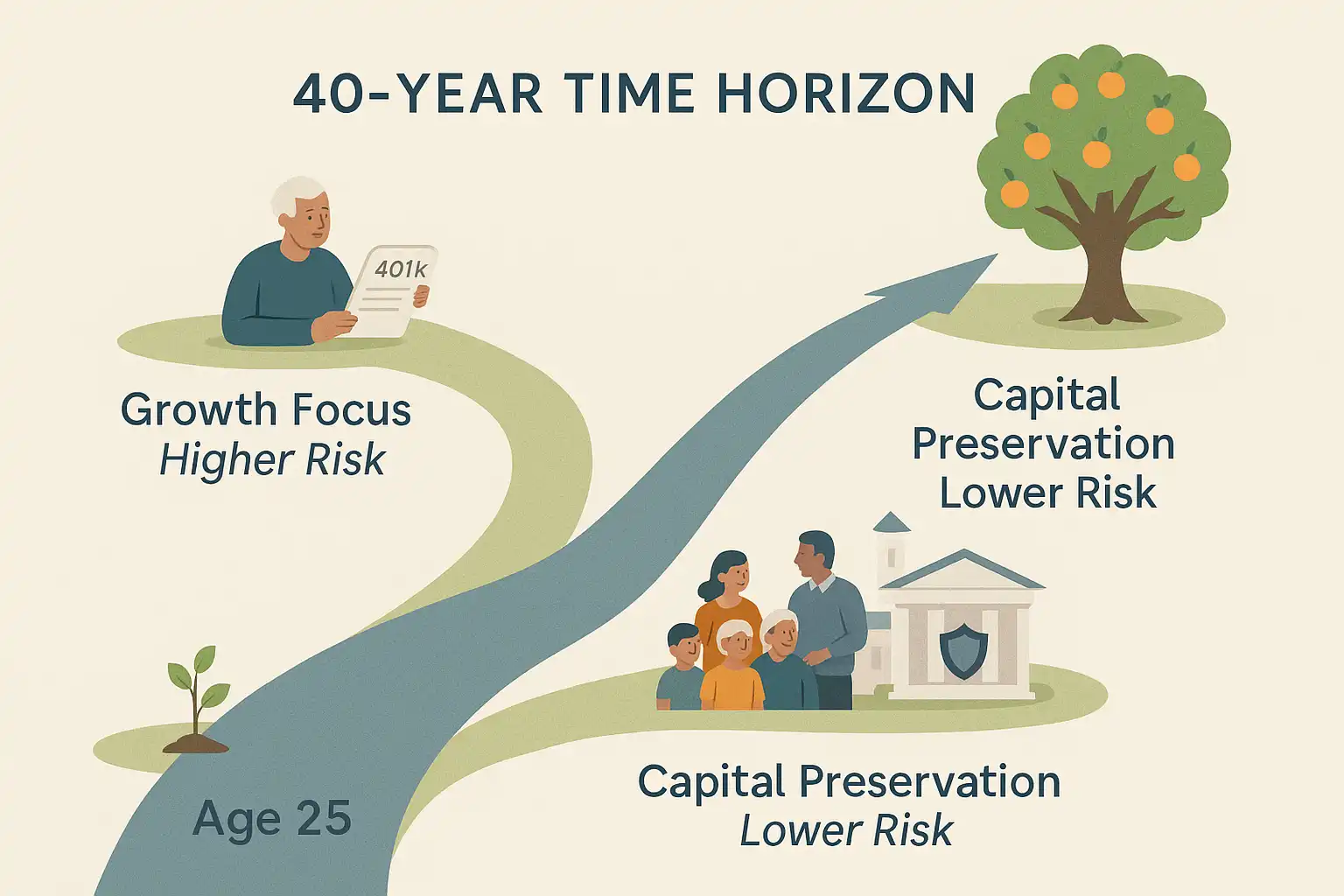

When you begin your financial journey, you’ll encounter one concept that is more profoundly important than any hot stock tip or economic headline: the investment time horizon.

More than almost any other factor, your time horizon dictates your investment strategy, how much risk you can take, and the total growth potential of your money. In this guide, we’ll explore why time is your greatest superpower and how to optimize it for 2026 and beyond.

1. What is a Time Horizon?

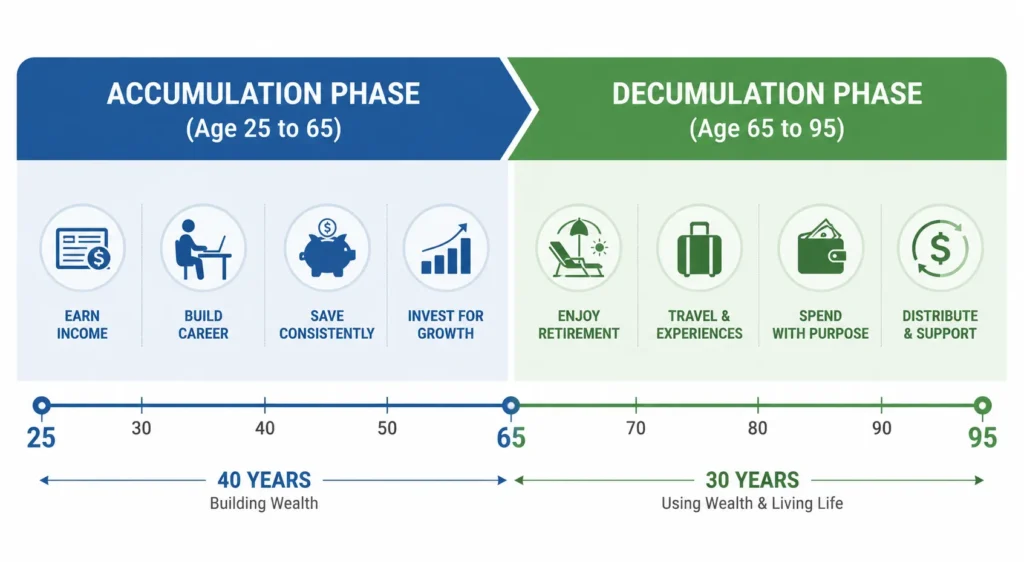

In investing, a time horizon is simply the total length of time you expect to hold an investment before you need to withdraw the money. For long-term planning, professionals break this into two critical phases:

- The Accumulation Time Horizon: The period when you are working and saving. For a 25-year-old, this is roughly 40 years. For a 50-year-old, it might be 15 years.

- The Decumulation Time Horizon: The period during retirement when you are withdrawing money to live on. Crucial Tip: Your time horizon doesn’t end the day you retire. A 65-year-old still has a decumulation horizon that could span 30 years or more.

2. Why Your Time Horizon is a “Superpower”

A long time horizon (10+ years) is your greatest financial asset. Here is how it fundamentally changes the rules of the game:

A. It Increases Your Risk Capacity

Market volatility is a short-term phenomenon. While the stock market can have a “bad year” where it drops 20%, those drops are historically smoothed out over long periods. With a 30-year horizon, you have the risk capacity to weather these storms and capture the higher returns offered by growth assets like stocks.

B. It Maximizes Compound Interest

Compound interest needs time to work its “magic.” Every extra year you give your portfolio allows your returns to generate their own returns, leading to exponential growth. In 2026, where market returns may be more moderate, the duration of your investment becomes the primary driver of wealth.

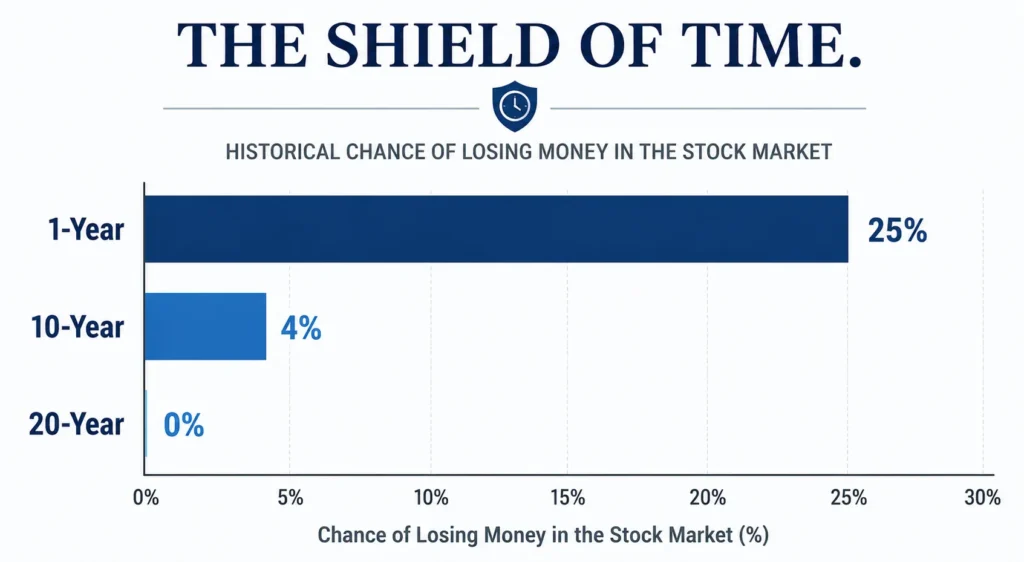

C. The Shield of Rolling Returns

Historical data proves that time heals all market wounds. * 1-Year Horizon: The odds of the S&P 500 being down are roughly 1 in 4.

- 10-Year Horizon: The odds of loss drop significantly.

- 20-Year Horizon: Historically, there has never been a 20-year period where the total return of the S&P 500 was negative.

3. How Time Horizon Shapes Your Strategy

To keep things simple, investors generally fall into one of three buckets. As your horizon changes, your strategy must evolve through what planners call a glide path.

Short-Term Horizon (0–3 Years)

- Goals: Wedding, house down payment, or an emergency fund.

- Strategy: Preservation of capital. In a “higher-for-longer” interest rate environment, your best friends are High-Yield Savings Accounts (HYSAs), Short-Term CDs, and Money Market Funds.

- Risk: Very Low. You don’t have time to wait for the stock market to recover if it crashes tomorrow.

Plan Your Short-Term Bucket: Not sure how much cash you need to keep safe from market drops? Use our Free Emergency Fund Calculator to find your exact target.

Medium-Term Horizon (3–10 Years)

- Goals: Starting a business, buying a second home, or college tuition for a teenager.

- Strategy: Balanced growth. A conservative mix of broad market Index Funds and Investment-grade bonds.

- Risk: Moderate. You can handle some fluctuations, but you should begin shifting toward “safer” assets as you get closer to the 3-year mark.

Long-Term Horizon (10+ Years)

- Goals: Retirement, building generational wealth.

- Strategy: Aggressive growth. This is where you harness the “superpower” of Total Stock Market Index Funds and let compound interest do the heavy lifting.

- Risk: High (Volatility). Because you have a decade or more, “paper losses” during a market dip don’t matter—only the final value at the end of the horizon.

Special Case: The Retiree (In Decumulation)

- Expert Insight: Retirees often make the mistake of becoming too conservative. Because you may spend 30 years in retirement, you still need growth to stay ahead of inflation.

- The Fix: Use a “Bucket Strategy.” Keep 2 years of cash for short-term needs, 5 years of bonds for the medium term, and the rest in stocks to fund your later years.

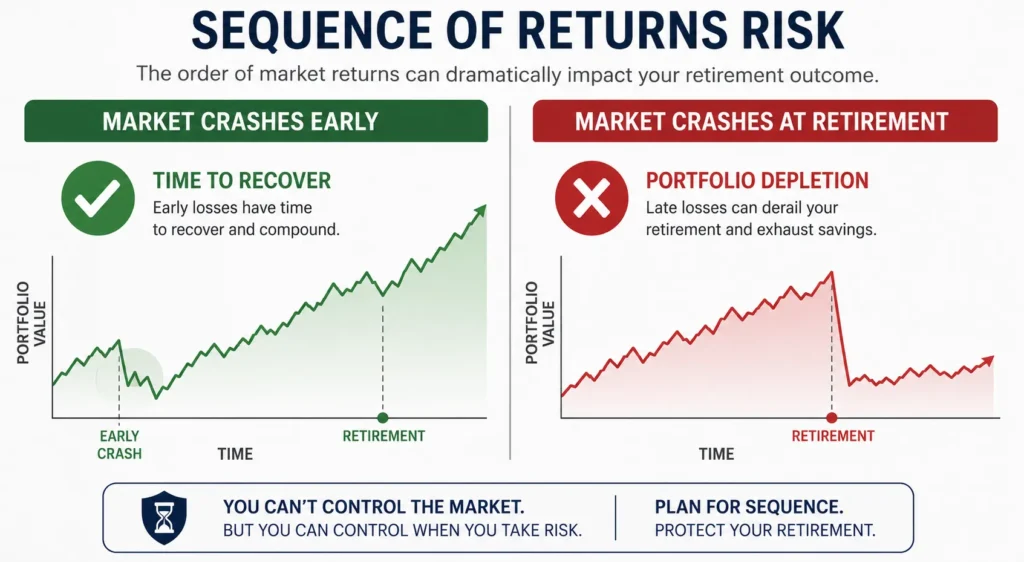

4. Sequence of Returns Risk: The Hidden Danger

In 2026, investors must be aware of Sequence of Returns Risk. This is the risk that a market crash occurs just as you enter the decumulation phase.

- Scenario A: You have a crash 10 years before you retire. You recover.

- Scenario B: You have a crash in Year 1 of retirement. Since you are withdrawing money while the market is down, your portfolio is depleted at an accelerated rate.

Your Defense: As your horizon shortens, your need for liquidity (cash/short-term bonds) increases to ensure you never have to sell stocks at a loss.

5. Conclusion: Aligning Your Goals

Understanding your time horizon is the essential first step in crafting a successful strategy.

- If you’re young: Embrace volatility as a tool for growth.

- If you’re mid-career: Audit your glide path to ensure you aren’t taking too much (or too little) risk.

- If you’re retired: Remember that your horizon is still decades long, and your portfolio needs to keep pace with inflation.

By aligning your investment choices with your time horizon, you move from “guessing” the market to “owning” your financial future.

Disclaimer: This guide is for educational purposes. Consult with a Certified Financial Planner (CFP) to tailor a strategy to your specific needs.

Jaiveer Hooda is a personal finance researcher and the founder of Grow Your Money Smart. With a background in computer engineering, he approaches money the way an engineer approaches any complex system — through data analysis, mathematical modeling, and ruthless optimization.

He built this platform on a single conviction: financial freedom is not a matter of luck. It is a system that can be designed, tested, and executed by anyone willing to follow the right blueprint. Every strategy published here is researched to the numbers, not written to the trend.

Expertise: Debt elimination · Retirement planning · Passive income · Budgeting systems

Connect: Pinterest | growyourmoneysmart.com | Contact Us